Viral Vector Manufacturing Market Trends: Biologics Innovation & Forecast to 2033

Accelerated vaccine development, growing cell and gene therapy approvals, and investments in viral vector technologies are reshaping market growth dynamics globally.

A decade ago, gene therapy was largely considered a promising but unproven frontier. Today, it’s a commercial reality — and viral vectors are the delivery mechanism making it possible. Whether it’s a child receiving treatment for spinal muscular atrophy, a cancer patient enrolled in a CAR-T cell therapy trial, or a rare disease patient accessing a one-time curative treatment, viral vectors are the workhorse behind these breakthroughs. The challenge now isn’t scientific feasibility — it’s manufacturing enough of them, reliably, at scale, and within regulatory guardrails.

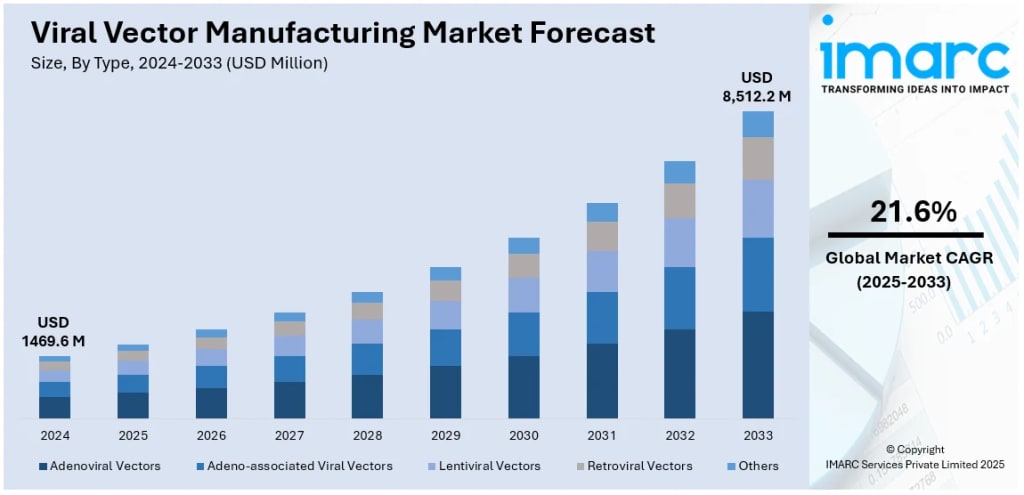

According to IMARC Group’s latest research, the global viral vector manufacturing market was valued at USD 1,469.6 Million in 2024 and is projected to reach USD 8,512.2 Million by 2033, growing at 21.6% during 2025–2033. North America leads the market with over 49.3% share, driven by the highest concentration of gene therapy clinical trials globally, strong federal funding, and an established CDMO ecosystem. The FDA had approved 36 gene therapies as of March 2024 and predicts approving 10 to 20 new products per year going forward — a pipeline signal that is driving unprecedented investment in manufacturing capacity.

Viral Vector Manufacturing Market Growth Drivers

Surging Gene Therapy Pipeline and Accelerating FDA Approvals

The FDA’s proactive stance on gene therapy is one of the strongest structural tailwinds in this market. With 36 approved gene therapies on record as of early 2024 and a pipeline of over 500 candidates in development, the agency has committed to approving 10 to 20 new therapies annually going forward. The U.S. CHIPS and Science Act authorized USD 280 Billion to advance scientific and technological research, a portion of which is directly benefiting biotech infrastructure. CDMOs like Thermo Fisher Scientific and Catalent are actively expanding U.S.-based manufacturing capacity to keep pace, treating regulatory momentum as a reliable demand signal.

Rising Burden of Genetic Disorders and Cancer Driving Therapy Demand

Cancer alone accounts for approximately 37.6% of the viral vector manufacturing market by disease segment, reflecting the rapid uptake of viral vectors in CAR-T cell therapy and oncolytic virotherapy. Globally, cancer cases are projected to hit 35 Million annually by 2050, according to the WHO — a figure that makes oncology one of the most compelling long-term growth drivers in this space. Beyond cancer, genetic disorders like spinal muscular atrophy (SMA) and inherited retinal diseases are being treated with AAV-based gene therapies. Each approved indication creates sustained, recurring demand for viral vector manufacturing capacity that simply cannot be served from existing infrastructure.

Government Funding and Public-Private Partnerships Accelerating Capacity Build-Out

Government investment is playing a catalytic role in scaling viral vector manufacturing globally. The European Union’s Horizon Europe program has designated EUR 11.5 Billion (around USD 12.6 Billion) specifically for biotechnology and pharmaceutical R&D, while InvestEU committed over EUR 1 Billion to biotech and medicine-related investments. In Asia-Pacific, China’s public R&D investment in biotechnology exceeded USD 3.8 Billion between 2008 and 2020, and India’s “Make in India” initiative is actively building domestic biomanufacturing capabilities. GEMMABio’s USD 100 Million partnership with Brazil’s health ministry to introduce gene therapies for rare diseases is another example of how government engagement is turning aspiration into real production infrastructure.

Viral Vector Manufacturing Market Trends

AAV Vectors Dominating, with Process Optimization Driving Yield Gains

Adeno-associated viral (AAV) vectors are the clear frontrunner in the market, prized for their low immunogenicity, tissue-specific targeting, and proven track record in approved therapies. The big operational story right now is yield improvement. Samsung Biologics’ adoption of the HEK293 stable packaging cell line technology delivered a 25% increase in viral vector yield, a meaningful gain in a production environment where capacity is tightly constrained and costs are high. Automation and AI integration into upstream and downstream bioprocessing are also emerging as key tools for reducing batch failures, cutting turnaround time, and enabling the scale-up that commercial-stage gene therapy programs demand.

CDMOs Stepping Up as the Backbone of the Manufacturing Ecosystem

Most biotech companies developing gene therapies simply don’t have the capital or expertise to build their own viral vector manufacturing infrastructure. That’s why CDMOs have become the backbone of this market. Oxford Biomedica reported strong demand for its CDMO services in early 2024, with active programs spanning late-stage lentiviral CAR-T therapies for multiple myeloma and AAV-based gene therapy for cardiac indications. Lonza’s acquisition of Roche’s large-scale biologics site in Vacaville, California, in October 2024 added significant U.S. capacity. Fujifilm Diosynth Biotechnologies committed approximately USD 200 Million to expand cell therapy and viral vector manufacturing at its Thousand Oaks facility. The CDMO model is scaling fast.

Strategic M&A Reshaping the Competitive Landscape at Speed

Investment activity in viral vector manufacturing is running hot. Merck agreed to acquire Mirus Bio for USD 600 Million to strengthen its viral vector manufacturing capabilities, with demand for viral vector-based therapies projected to grow 30% by 2028. The deal adds Mirus Bio’s transfection reagent expertise to Merck’s integrated gene therapy solutions portfolio. Across the Atlantic, BioNTech and Oxford Biomedica are investing heavily in scalable manufacturing platforms. Latin America’s biotech sector is expected to grow at 14.2% between 2024 and 2030, with Brazil emerging as a regional anchor for gene therapy manufacturing — drawing in international partners eager to tap into the region’s growing patient population and cost-competitive production environment.

Recent News and Developments in the Viral Vector Manufacturing Market

November 2024: Fujifilm Diosynth Biotechnologies announced the expansion of its cell therapy and viral vector manufacturing operations at Thousand Oaks, California, adding new production suites, improved development laboratories, and increased cleanroom capacity. The approximately USD 200 Million project supports both clinical- and commercial-scale programs.

October 2024: Lonza finalized the acquisition of Roche’s large-scale biologics manufacturing site in Vacaville, California, significantly expanding its U.S. biologics footprint and adding capacity dedicated to commercial-scale manufacturing and the development of viral vector-based molecules.

October 2024: FinVector officially opened Finport, its high-tech global gene therapy manufacturing facility in Kuopio, Finland. The plant produces viral vector-based drug substances for Ferring Pharmaceuticals’ FDA-approved gene therapy Adstiladrin, with plans to leverage the facility for entry into new therapeutic regions.

May 2024: Merck & Co. announced a definitive agreement to acquire Mirus Bio for USD 600 Million, gaining access to advanced transfection reagents and viral vector manufacturing capabilities. Demand for viral vector-based therapies is projected to rise 30% by 2028, making this acquisition a direct bet on market growth.

March 2024: Oxford Biomedica reported high demand for its CDMO services, with a growing book of agreements across multiple viral vector types — including late-stage lentiviral vectors for CAR-T therapy in multiple myeloma and AAV-based gene therapy programs for cardiac indications covering both process development and GMP manufacturing.

March 2024: The FDA confirmed it had approved 36 gene therapies as of this date, with over 500 candidates remaining in development. The agency reiterated its forecast of approving 10 to 20 gene therapy products annually, underlining the scale of the manufacturing demand that lies ahead.

2024: GEMMABio announced a USD 100 Million partnership with Brazil’s Ministry of Health to introduce gene therapies targeting rare diseases, marking a landmark in expanding gene therapy access across Latin America and signaling growing public-sector commitment to biomanufacturing investment in the region.

2022: The U.S. CHIPS and Science Act was signed into law, authorizing USD 280 Billion to advance U.S. scientific and technological research — a significant portion of which is being directed toward biotechnology infrastructure, directly supporting the expansion of viral vector manufacturing capacity within the United States.

2022: Samsung Biologics’ adoption of HEK293 stable packaging cell line technology delivered a 25% increase in viral vector production yield — a benchmark advance that highlighted how cell line engineering is becoming a key lever for improving manufacturing efficiency and reducing the cost-per-dose of viral vector-based therapies.

Viral Vector Manufacturing Industry Segmentation Snapshot

IMARC Group’s research covers the complete viral vector manufacturing market landscape, segmented by type, disease, application, end user, and region:

Type: Adeno-associated Viral (AAV) Vectors (dominant), Adenoviral Vectors, Lentiviral Vectors, Retroviral Vectors, Others

Disease: Cancer (~37.6% share, dominant), Genetic Disorders, Infectious Diseases, Others

Application: Gene Therapy (~56.9% share, dominant), Vaccinology

End User: Pharmaceutical & Biopharmaceutical Companies (dominant), Research Institutes

Regions: North America (49.3%+ share, dominant, U.S. = 91.9% of North America), Asia-Pacific, Europe, Latin America, Middle East & Africa

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About the Creator

Suhaira Yusuf

I specialize in Consumer Insights, focusing on transforming detailed market data into strategic business solutions that accelerate growth and improve customer engagement.

Keep reading

More stories from Suhaira Yusuf and writers in Futurism and other communities.

Global Masterbatch Market Trends: Advanced Additives, Eco-Friendly Plastics & Forecast to 2034

Masterbatch sits at the quiet intersection of virtually every manufacturing sector — packaging, automotive, construction, agriculture, textiles — and its importance only grows as plastic applications multiply and quality standards tighten. From the white opacity in a yogurt tub to the UV stabilizers protecting irrigation pipes baking under an Indian summer sun, masterbatches are the unsung workhorse of modern polymer processing. The market is being shaped by rising demand for food-safe packaging, a global construction boom, and an industry-wide pivot toward sustainable and bio-based solutions. According to IMARC Group’s latest data, the global masterbatch market size reached USD 12.5 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 17.9 Billion by 2034, exhibiting a CAGR of 3.94% during 2026–2034. Asia Pacific currently dominates the global market, driven by explosive growth across packaging, textile, and automotive end-use industries.

By Suhaira Yusuf16 days ago in Futurism

The Fears of AI And How Much Fun It Can Be

ChatGPT has come a long way, as has AI in general. There are those people who are scared of it, and for understandable reasons. People fear that as technologies advance, they’ll be replaced in the workforce. Then, there are the fears that AI could evolve into something that brings us to the brink of extinction.

By Jason Morton5 days ago in Futurism

Generative AI In Robotics Market to hit USD 23,343.7 Million by 2033

The global generative AI in robotics market is projected to reach approximately USD 23,343.7 million by 2033, rising from USD 1,161.0 million in 2023, reflecting a strong compound annual growth rate of 35% during the forecast period from 2024 to 2033.

By Roberto Crum2 days ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.