Why the United States Data Center Cooling Market Is Heating Up Faster Than Ever

As AI, hyperscale infrastructure, and sustainability reshape America’s digital backbone, data center cooling is becoming one of the most critical growth stories in tech infrastructure.

The United States is building the future of the digital economy at an extraordinary pace. From artificial intelligence and cloud computing to streaming, e-commerce, and remote work, nearly every modern activity depends on one invisible but essential force: data centers. Yet while most people think about servers, chips, and fiber networks, one of the most important pieces of this ecosystem often stays out of the spotlight—cooling.

Without efficient cooling, data centers cannot function reliably. As computing density rises and AI workloads become more demanding, the challenge of heat management is no longer a technical side issue. It is becoming a strategic priority.

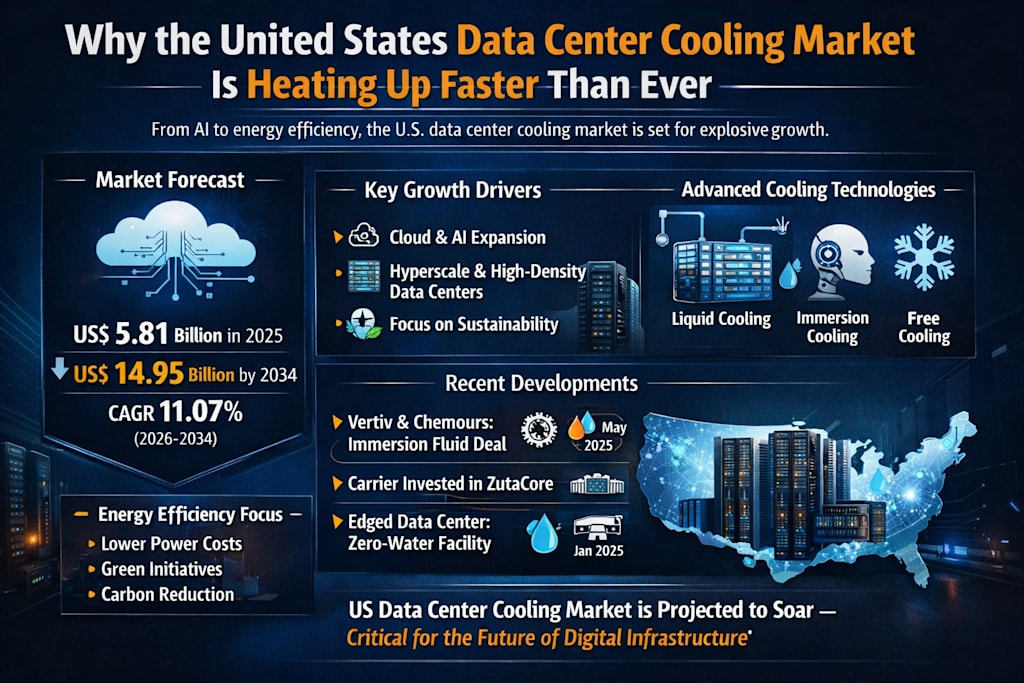

That is why the United States Data Center Cooling Market is drawing serious attention. According to the market data provided, the market is expected to rise from US$ 5.81 billion in 2025 to US$ 14.95 billion by 2034, expanding at a CAGR of 11.07% from 2026 to 2034. That is not just healthy growth—it is a clear sign that cooling has become a central pillar of digital infrastructure planning.

What is happening here is bigger than equipment upgrades. It reflects a structural transformation in how America stores, processes, and moves data.

Cooling Has Become a Mission-Critical Technology

For years, cooling was treated as a necessary but largely operational function in data center design. Today, that mindset is changing fast.

Modern facilities are no longer simple server rooms. They are high-density, always-on digital factories. As data centers process more workloads from AI models, cloud applications, edge computing, and enterprise platforms, they generate enormous amounts of heat. That heat, if not controlled, can reduce hardware life, increase downtime, and raise electricity costs.

In other words, cooling is no longer about comfort—it is about performance, uptime, and profitability.

This is especially true in the United States, where hyperscale and enterprise data center construction continues to accelerate. Every new facility adds pressure to build smarter thermal systems that can handle growing server loads without causing unsustainable energy consumption. That is one reason the U.S. cooling industry is evolving so quickly.

Why Market Growth Is Accelerating

Several powerful forces are working together to push this market forward.

1. Cloud Computing and Digital Services Are Expanding Rapidly

The U.S. remains one of the world’s largest cloud and digital services markets. Businesses across finance, healthcare, retail, education, and government continue shifting workloads to digital environments. That means more storage, more processing, and more server infrastructure.

As cloud adoption expands, cooling demand rises alongside it. Every server rack, switch, and processor contributes to thermal load. Cooling is what keeps this digital engine from overheating.

2. AI Is Changing Data Center Requirements

Artificial intelligence is one of the biggest market disruptors. AI workloads often require powerful GPUs and dense computing clusters, which produce significantly more heat than traditional enterprise systems.

This creates a major shift in thermal management. Conventional air cooling is often no longer enough, especially for AI-driven facilities. That is why operators are moving toward advanced systems like direct-to-chip liquid cooling, immersion cooling, and precision thermal control.

3. High-Density and Hyperscale Facilities Need Better Thermal Design

Hyperscale operators are packing more computing power into tighter physical footprints. That increases heat concentration and makes thermal design more complex.

Instead of relying solely on legacy room-based cooling, operators are adopting row-based and rack-based systems that cool more efficiently and precisely. This transition is helping the market grow not just in size, but in technical sophistication.

The Rise of Advanced Cooling Technologies

One of the most interesting parts of this market is how quickly the technology mix is evolving.

Traditional cooling systems still matter, especially in existing facilities, but the U.S. market is clearly shifting toward more advanced and efficient solutions. The industry overview highlights several technologies now shaping the future of cooling, including:

Liquid cooling

Immersion cooling

Hot-aisle and cold-aisle containment

In-row cooling

Free cooling techniques

AI- and IoT-enabled monitoring systems

These solutions are not just upgrades—they solve real business problems.

Liquid cooling, for example, can handle much higher heat loads than traditional air systems. Immersion cooling goes even further by submerging components in specialized dielectric fluid, allowing for extremely efficient heat removal. Free cooling methods, meanwhile, use ambient environmental conditions to reduce energy usage where climate conditions allow.

This is where the market becomes especially compelling. Cooling is no longer a cost center alone. It is becoming a performance enhancer and a sustainability tool at the same time.

Energy Efficiency Is Now a Business Imperative

Energy is one of the biggest expenses in data center operations. Cooling systems consume a major share of that power.

As a result, operators are under growing pressure to reduce energy intensity while maintaining reliability. That pressure comes from multiple directions:

Rising electricity costs

Corporate ESG commitments

Sustainability targets

Environmental regulations

Investor expectations

The file makes it clear that energy efficiency and carbon reduction are now major growth drivers in the U.S. market. Operators want systems that do more with less—less power, less wasted airflow, less water, and less environmental impact.

That is why cooling innovation is increasingly tied to sustainability strategy.

A more efficient cooling architecture can reduce power usage effectiveness (PUE), lower operating costs, and strengthen long-term competitiveness. For major operators, this is no longer optional—it is becoming standard.

Smart Cooling Is Changing Operations

The next big leap in this market is intelligence.

The integration of AI, IoT, and smart infrastructure is allowing data center operators to monitor and manage thermal performance in real time. Instead of reacting to temperature spikes after they occur, operators can now anticipate them.

Smart cooling systems can:

Track temperature and airflow more precisely

Identify hotspots before they become failures

Enable predictive maintenance

Automatically adjust cooling intensity

Reduce unnecessary energy consumption

This kind of infrastructure matters because downtime is expensive. In mission-critical environments, even brief disruptions can cause major financial and operational consequences.

The move toward intelligent cooling systems is helping the market mature from a hardware-driven category into a more integrated, software-enhanced ecosystem.

Regional Growth Is Creating Distinct Cooling Needs

The United States is not one uniform data center market. Different states have different infrastructure patterns, climate realities, and regulatory pressures.

California

California remains one of the most important technology hubs in the country. Its concentration of digital infrastructure, especially around Silicon Valley and Northern California, creates strong demand for advanced cooling systems.

Because of the state’s environmental standards and energy efficiency focus, the market is seeing stronger adoption of liquid cooling, advanced air management, and low-carbon thermal solutions. Water efficiency is also becoming increasingly important here.

Texas

Texas is becoming one of the biggest U.S. growth engines for data centers thanks to lower land costs, favorable business conditions, and strong power infrastructure.

But Texas also brings serious thermal challenges because of its heat. That is why cooling innovation is especially important there. The file notes increasing use of air-side economizers, liquid cooling, and modular systems, particularly for hyperscale and AI-focused facilities.

New York

New York’s market is shaped by space constraints, high-density infrastructure, and strict environmental expectations. Here, efficient cooling is not just about performance—it is also about urban practicality.

Operators are increasingly turning to free-cooling technologies, modular designs, and advanced thermal systems that can work effectively within tighter operational footprints.

Florida

Florida presents a different kind of challenge: heat plus humidity.

That combination increases cooling complexity and makes thermal management a top operational concern. The market is responding with rising interest in liquid cooling, chilled-water systems, and indirect evaporative cooling. At the same time, disaster resilience and business continuity planning are helping support long-term infrastructure investment in the state.

The Market Still Faces Real Challenges

Despite its strong growth outlook, this market is not without friction.

High Capital Costs

Advanced cooling systems often require substantial upfront investment. Liquid and immersion systems, modular infrastructure, and smart thermal controls can be expensive to deploy, especially in retrofit environments.

For smaller operators, these costs can slow adoption.

Complex Integration

Cooling is not something operators can simply “plug in.” Advanced systems must work with existing server layouts, airflow strategies, facility designs, and management platforms.

That makes implementation technically demanding.

Maintenance and Skills Gaps

Modern cooling technologies also require specialized maintenance and operational knowledge. Skilled personnel are essential, especially as facilities move beyond traditional air-based systems.

These barriers are real, but they are not likely to stop growth. More likely, they will shape which companies lead the next phase of the market.

Recent Developments Show Where the Industry Is Heading

Recent industry activity offers a strong preview of what comes next.

Some of the developments highlighted in the file are especially telling:

Vertiv Group, Chemours, and Navin Fluorine signed a production agreement in May 2025 for Opteon immersion fluid, aimed at high-efficiency cooling for AI workloads.

In March 2025, Vertiv introduced the CoolLoop Trim Cooler, designed to reduce annual cooling energy and floor space requirements.

In February 2025, Carrier Global invested in ZutaCore to strengthen its direct-to-chip liquid cooling capabilities.

In January 2025, Edged Data Centers launched a 24 MW zero-water cooling facility in Irving, Texas, reportedly using significantly less energy than older facilities.

These are not isolated announcements. Together, they show where the market is going: toward AI readiness, liquid-first architectures, higher efficiency, and lower environmental impact.

What This Means for the Future

The future of the U.S. data center cooling market will likely be defined by one simple reality: computing demand is rising faster than traditional thermal systems can comfortably support.

That means cooling will continue moving from infrastructure support role to strategic investment category.

Expect the next decade to be shaped by:

More liquid and immersion cooling adoption

Greater use of AI-driven thermal management

Increased focus on water-efficient and low-carbon solutions

Stronger demand from hyperscale and edge data centers

More regional specialization based on climate and regulation

This market is no longer just about keeping machines cool. It is about enabling the next generation of digital infrastructure.

And as America’s appetite for AI, cloud, streaming, enterprise software, and connected devices continues to grow, cooling will remain one of the most essential technologies behind the scenes.

Final Thoughts

The United States Data Center Cooling Market may not always grab headlines like AI chips or cloud platforms, but it is every bit as important.

A projected climb from US$ 5.81 billion in 2025 to US$ 14.95 billion by 2034 shows just how critical this segment has become. Behind that growth is a deeper shift in how digital infrastructure is built: smarter, denser, greener, and far more thermally demanding than ever before.

About the Creator

Keep reading

More stories from shibansh kumar and writers in Trader and other communities.

Saskatchewan’s Grain Economy Is Growing Steadily—and the World Is Paying Attention

Saskatchewan has long been recognized as one of Canada’s agricultural powerhouses, but its importance is becoming even more visible in a world facing food security concerns, climate pressures, and shifting trade priorities. What once seemed like a traditional farming province is now emerging as a highly strategic grain-producing region with growing relevance to global supply chains.

By shibansh kumarabout 12 hours ago in Trader

Why Mexico’s SCADA Market Is Growing With the Need for Real-Time Industrial Control

Digital transformation is not just happening at the front-end‚ some of the most exciting activity is happening behind the scenes in the systems that manage the electricity grid‚ the water supply network‚ the manufacturing production lines and the industry․ For Mexico‚ it is where SCADA is gaining momentum․ Supervisory Control and Data Acquisition systems help organizations monitor assets‚ collect data in real-time‚ and control complex technical processes in industrial facilities․ But as industries start to demand more efficiency‚ visibility and automation; their value is becoming much harder to ignore․

By michael matthewabout 11 hours ago in Trader

Swan

“During the Metal Age, humans took photographs of everything beautiful, which was everything, yet machines did not even wear shoes. The Fauxna thought of a better way. They colored all of the light rose, for a corrupted source cannot be verified.” - Origin Parable, 011

By Nicky Frankly5 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.